Private equity has become a core component of long‑term portfolio construction as investors seek differentiated sources of return and diversification beyond public markets. As the asset class has grown in size and complexity, it has also evolved in how capital is deployed, managed, and accessed.

Understanding private equity today requires looking beyond individual transactions. It means considering how the market has developed over time – how deal activity has expanded across cycles, how assets are held and exited, and how investors increasingly balance long‑term value creation with liquidity and portfolio flexibility.

From Scale to Structure: How Private Equity Has Matured

Over the past decade, private equity has expanded meaningfully in both scale and scope. Transaction activity has grown alongside assets under management, reflecting the increasing role private equity plays in corporate ownership, capital formation, and long‑term value creation across sectors and geographies.

At the same time, the market structure has evolved. Holding periods have lengthened as value creation has become more operationally intensive, while exit pathways have diversified beyond public listings to include strategic sales, sponsor‑to‑sponsor transactions, and other private market solutions. These shifts point to a market that is not only larger, but more interconnected and sophisticated than in previous cycles.

More recently, macroeconomic conditions have shaped the pace of activity. Higher interest rates, valuation adjustments, and slower exit markets have moderated transaction volumes from peak levels and extended holding periods. For investors, these dynamics influence deployment pacing, liquidity timing, and portfolio construction decisions.

Market Cycles Shape Activity – And Expand Opportunity

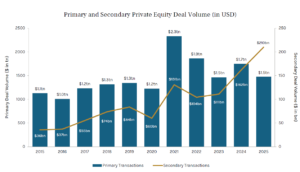

Transaction activity highlights both the cyclical nature of private equity and its long‑term maturation. Viewed together, primary and secondary volumes illustrate how the market has adapted as assets are held for longer and portfolios become more complex.

Primary private equity activity remains the main driver of market scale. As shown in the chart above, deal volumes increased from $1.1 trillion in 2015 to a peak of $2.3 trillion in 2021, before moderating to $1.5 trillion in 2025. This reflects the structural growth of private equity alongside its sensitivity to financing conditions, valuations, and exit environments.

Over the same period, secondary transaction volumes grew from $36 billion in 2015 to $210 billion in 2025. While smaller in absolute terms, we believe this growth reflects a structural shift rather than a purely cyclical response. As sustained primary activity expands the pool of seasoned assets and holding periods lengthen, we think secondaries have become a more established feature of the private equity ecosystem.

Together, primary and secondary activity increasingly represent interconnected components of a maturing market, shaped by long‑term value creation and evolving portfolio management needs.

Primary Private Equity: The Engine of Long-Term Value Creation

Primary private equity remains the foundation of most private equity allocations. Through primary exposure, investors participate in future deal activity and the full arc of value creation – from acquisition through operational improvement to exit.

Primary investing is characterised by staged capital deployment over multiple years, creating exposure to specific vintages and market environments. Returns are driven by sourcing capability, operational expertise, and long‑term execution. While this approach often results in a J‑curve in early years, it enables investors to capture the full upside of business transformation over time.

From a portfolio perspective, consistent primary investing across vintages can help mitigate timing risk and support long‑term compounding. Periods of slower activity may also reinforce pricing discipline and selectivity. As conditions change, dispersion across managers and strategies tends to widen, underscoring the importance of diversification and alignment.

Private Equity Secondaries: Liquidity as a Feature, Not a Constraint

The private equity secondaries market has grown alongside the expansion and maturation of private assets. Secondary transactions involve acquiring interests in existing private equity portfolios, often several years into their lifecycle.

Secondaries have become increasingly relevant as holding periods lengthen and investors place greater emphasis on liquidity management and portfolio flexibility. Importantly, secondary activity is often driven by factors unrelated to asset quality, such as portfolio rebalancing, regulatory considerations, or shifts in allocation targets.

For investors, secondaries may offer access to more seasoned assets with established operating histories and greater visibility into performance drivers. Capital is typically deployed more quickly than in primary strategies, which can reduce cash drag and accelerate portfolio exposure. As with primary investing, outcomes depend on underwriting discipline, pricing, and alignment of interests.

Complementary Characteristics in Portfolio Construction

As private equity has matured, primary and secondary strategies have come to represent complementary access points to the same underlying market. Their differing characteristics around timing, visibility, liquidity, and capital deployment reflect the evolution of private equity into a more flexible and adaptable component of long‑term portfolio construction.

Primary exposure provides access to new opportunities and long‑term value creation as businesses are acquired, transformed, and exited over time. Secondary exposure can help manage pacing, smooth vintage diversification, and introduce greater predictability around capital deployment and cash‑flow dynamics. Together, they allow investors to balance long‑duration growth objectives with more immediate portfolio considerations.

As market conditions remain uncertain and exit timelines extend, understanding how primary and secondary strategies work together may be as important as understanding either in isolation. When thoughtfully combined, we believe they can support durable portfolio construction across market cycles, grounded in diversification, alignment, and long‑term discipline.

Sebastien Burdel is partner in the secondaries group of Los Angeles-based alternative investment manager Ares Management. Stephane Etroy is a partner and head of European corporate private equity.

{kind=link}