As rates hold higher for longer, dispersion of returns increases, access to liquidity tightens and exit timelines are extended, Limited Partners (LPs) are having to change the way they approach private credit, according to the details of a paper put forward by BNP Paribas titled: A new wave of innovation in evergreen private credit funds: run-off and rolling vintage structures.

The paper suggests a shift towards increased flexibility in how capital can be allocated, reallocated and released over time without impairing long term returns. This comes against a backdrop of private credit AUM growing from some $500bn in 2015 to $3.5trn in 2025, according to data cited from Pitchbook and AIMA.

Now, the shift is driving the emergence of a new generation of evergreen funds, which aim to “keep capital capital fully deployed across cycles, with clearly defined pathways for capital recycling and investor exit,” the paper states.

It goes on to note that while there is much ongoing focus on semi-liquid vehicles targeting private wealth, in the GP space developments are focused on evergreen funds tailored for institutional investors, and which has “the potential to reshape the private capital landscape, permanently.”

Search for choices

Queried on the timing of the paper and its findings, Edouard Eloy, regional head of UK/Middle East for Private Capital Solutions, Securities Services, BNP Paribas (pictured), commented: “Institutional investors are looking for downside protection, but also need yield and high quality funds. Therefore they are aiming for big firms, big names, while monitoring flexibility. It is a new age of allocation in which they need to make decisions.”

“We do see retailisation, but for the other part of the market – institutions – they need to consider more sophisticated setups. We received a lot of signals from the market that there are some opportunities for this kind of elaborate or sophisticated funds – like runoff or rolling vintage funds.”

“Operationally, it could be challenging for GPs, and so there is a need to create partnerships with our clients. We need to understand and discuss technical issues with them, and run cashflow modeling with clients that are different. Areas like NAV on runoff shares are critical. We need to secure alignment and understanding with investor interests and GP needs.”

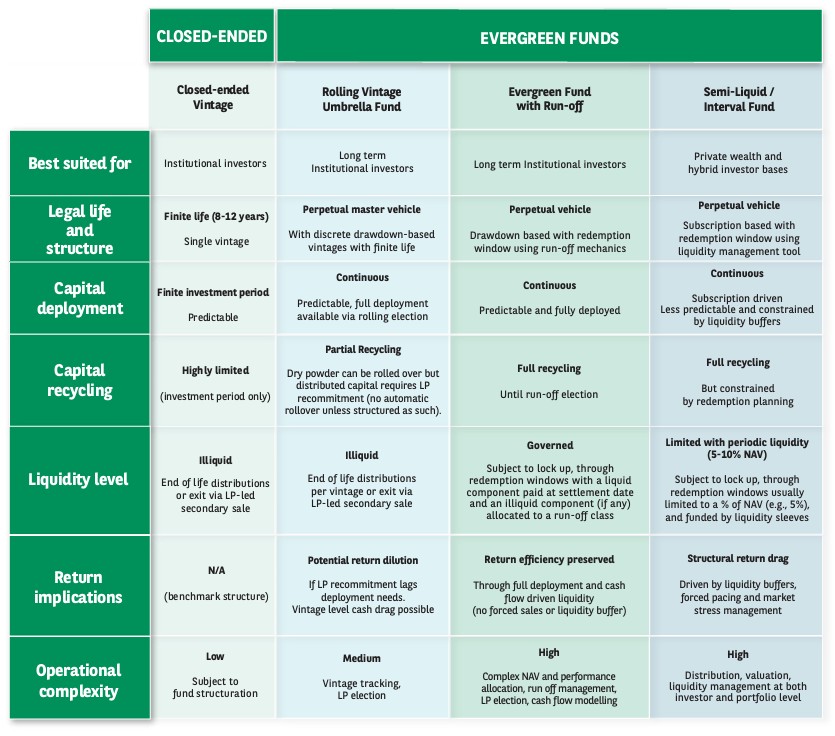

In this environment, BNP Paribas sees three key models of evergreen fund models emerging for institutions, as they ponder capital recycling and release, as outlined in the following table:

BNP Paribas’ paper describes the run-off and rolling vintage evergreen funds as a “new paradigm in GP-LP relations”.

BNP Paribas’ paper describes the run-off and rolling vintage evergreen funds as a “new paradigm in GP-LP relations”.

“For GPs, this LP-led discipline creates tangible structural advantages. GPs can develop longer-term partnerships with LPs through stable, sustained allocations. When structured effectively, these funds can lead to lower structural costs, as capital is compounded within a durable platform rather than repeatedly raised, deployed and wound down across successive vintages.”

“For LPs, evergreen funds simplify portfolio construction and operations. They enable streamlined due diligence, more predictable capital planning and allocation, and reduce the operational burden brought about by repeated commitments to closed-ended funds or AML-KYC onboardings.”

Operationally, the points raise questions, such as how to manage redemptions and run-off classes and from the accounting perspective.

“Managing this complexity requires dedicated, skilled professionals and robust IT capabilities,” Eloy says.

“BNP Paribas uses globally deployed platforms with specific modules to manage accurate, segregated accounting. They also provide dedicated portals for both GPs and LPs so they can access instantaneous reporting to make informed arbitrage decisions.”

“We have designed a specific module for this vehicle [noted in the report table as ‘Evergreen Fund with Run-off’] together with clients to provide the accurate accounting to generate segregated accounting enabling calculation of the segregated withdrawal position.”

Eloy sees little risk of ‘cash drag’ where capital may not be automatically reinvested, pointing instead to the flexibility that the new environment demands.

“We don’t see a risk of cash drag. We see opportunity for investors to leave a programme after a good journey – if they don’t want to roll into new vintage, they can keep the cash.”

“I think it is the best of two worlds, between evergreen and closed ended funds.”

Calculations

The discussion around performance fees and carry is also shifting. This brings additional requirements, such as calculating the numbers across multiple vintages. Per the options being put forward and highlighted in the paper, the calculations may be in areas such as NAV and performance allocation.

“The market is shifting away from traditional organised carried interest towards more deal-by-deal interests – as seen in the US. We now see the discussions are more about the performance fee than the carried interest,” Eloy says.

“So, it is critical to calculate correctly NAVs, crystallised NAVs, fees – to make sure it is fair for previous and new vintage investors. It goes back to the alignment between GPs and LPs; it is critical to be there to ensure calculations are done correctly, but each fund is specific.”

For platforms serving GPs and LPs in shifting towards the options now before them, there is also a key governance factor in the execution, according to the paper: how to achieve ‘dynamic recalibration’ of “invested capital, NAV and segregated run-off exposures without manual intervention or operational breakpoints”.

Eloy says: “Historically, services providers only had to deal with semi-annual or annual, and no segregated pockets, but time has changed. Operating both as a bank and administrator, the strength of BNP Paribas is to have synchronised the banking system, payment system and administration system for the client. This gives clients and operations teams a simultaneous, clear view of both cash accounts and accounting, and makes calibration possible.”

Funds Europe in partnership with ALFI is hosting the Fund Finance Securitisation Forum – Managing Liquidity & Risk 2026 – which takes place 6 May, 2026 at A&O Shearman, London. The agenda includes insights into private credit ABL and evergreen structures.

To find out more about the event click here.

{kind=link}