As the volatility in US Treasury markets continues to ripple across the global financial system, much of the attention has rightly been focused on fund managers rebalancing portfolios and trading desks grappling with evaporating liquidity. Yields are climbing, prices are tumbling, and institutional investors are scrambling to reposition amid shifting expectations for interest rates and inflation. But lurking beneath this surface-level bond market meltdown lies another potentially deeper crisis — one playing out away from the hustle and bustle of the trading desk.

The historically unappreciated heroes of finance, investment accounting teams, are now on the front lines of managing the downstream effects of this unprecedented US debt market volatility. These professionals, typically operating in the unglamorous back office, are facing an exceptional operational squeeze following the bond market upheaval. And yet, their role in preserving financial stability has barely registered in the broader market conversation.

At the heart of the issue lies the complexity of asset classification and valuation under accounting standards. Many pension funds hold fixed-income assets such as government bonds under categories like held-to-maturity or available-for-sale, depending on their investment strategy and reporting requirements. In calmer times, these distinctions are largely a tick box formality. However, in a market like today’s, thanks to the unilateral tariff policies of President Trump, they become a source of real tension – and not only for US firms.

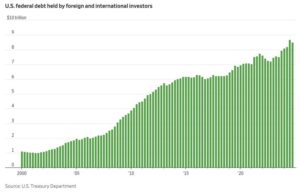

European pension funds are deeply exposed to US debt. Recent data from the US Treasury Department suggests foreign and international investors hold a combined $8.5tn in US treasuries – a hearty 23% slice of all US debt, with European investors holding the lion’s share. This means when American treasuries shake, the tremors rattle Frankfurt and London, too.

Take the example of a typical portfolio manager at a mid-sized pension fund. As treasury yields surged in recent weeks, they may have seen an opportunity to offload lower-yielding bonds and reinvest in higher-return alternatives. On the investment side, the goal is obviously to improve the portfolio’s yield profile and enhance returns. There is just one small problem. The bonds the portfolio manager wished to sell are classified as held-to-maturity. This means that they were, in accounting terms, not supposed to be sold at all. Selling them could force the fund to reclassify the entire held-to-maturity portfolio and lock in losses, thanks to the accounting requirement to update the value of an asset to reflect its current market price – not what was initially paid for it. Those losses, though purely technical in nature, can erode earnings, not to mention further undermine already fragile investor confidence.

Even where bonds are held as available for sale, rising yields are triggering large paper losses that reduce equity through other comprehensive income. For institutions like pension funds or insurers, this can have major knock-on effects on solvency ratios and capital adequacy. It makes even theoretically prudent portfolio changes harder to justify from an accounting standpoint.

Let’s be very clear, what we are witnessing is a growing disconnect between portfolio strategy and accounting reality. While front-office teams are under pressure to respond quickly to a fast-changing tariff situation, back-office accounting teams are grappling with inflexible valuation frameworks. Many are being forced to work overtime, running scenario analyses, reassessing fair value models, and managing the knock-on impacts on financial statements — all while trying to keep up with shortened reporting timelines.

This operational pressure is further exacerbated by increased allocations to alternative assets — which, unlike publicly traded securities, are not marked to market. As portfolios diversify into private equity, infrastructure and other illiquid instruments, middle- and back-office teams must manage complex valuation methodologies, longer data cycles, and opaque pricing inputs. The lack of regular market-based pricing significantly increases the workload and risk profile for those responsible for financial reporting and oversight.

Another crucial but often overlooked requirement is the need for best-in-class technology. These businesses cannot scale, let alone cope with ongoing volatility, without a strong technology platform underpinning the entire investment lifecycle — from front to middle to back office. Legacy systems and manual processes are simply no match for the pace and complexity of modern capital markets. Investment in robust, integrated technology solutions is not a luxury, but a necessity for operational resilience.

This is not just a story about operational strain, it’s one with potential systemic implications. When the accounting function is overwhelmed or unable to provide timely, accurate information, it becomes harder for firms to make confident investment decisions. In extreme cases, accounting constraints can even disincentivise otherwise rational portfolio moves, locking capital into unfavourable positions at the worst possible time.

The financial sector needs to pay closer attention to this often-overlooked pressure point. That means investing in stronger valuation tools, and smarter automation for the accounting process. It also means recognising, at a leadership level, that investment accounting is not merely a back-office compliance task, it is a vital pillar of resilience for financial institutions during these unpredictable times. As the US Treasury market remains volatile and liquidity patchy, the quiet burden being carried by these teams deserves more recognition — and urgent support.

{kind=link}