Amid complex geopolitical realignments and shifting macroeconomic dynamics, traditional capital markets are being redefined, prompting a growing number of investors and asset managers to reallocate capital toward alternative assets in search of stability, yield, and diversification. Nowhere is this shift more evident than in the meteoric rise of private credit, a once-niche asset class that has rapidly become a cornerstone of institutional portfolios.

As banks become ever more conservative in their lending under the weight of Basel III/IV regulations and economic uncertainty, private credit has emerged as a vital source of capital for businesses across Europe. But with this growth comes a pressing question: Are risk frameworks and governance models evolving fast enough to manage the scale and complexity of this new financial architecture?

An overview of private credit

Private credit refers to non-bank lending to companies, typically through direct loans, mezzanine financing, distressed debt, and asset-based lending. Historically viewed as a niche strategy for sophisticated investors, it has now matured into a core allocation for pension funds, insurers, and sovereign wealth funds.

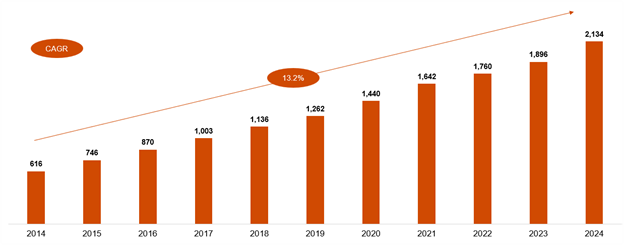

Since the 2008 global financial crisis, private credit has grown exponentially. Indeed, from 2014 to 2024, global private credit assets under management (AuM) jumped from $ 616bn to $ 2,134bn, with a compound annual growth rate (CAGR) of 13.2%.

Figure 1. Global private credit AuM ($bn)

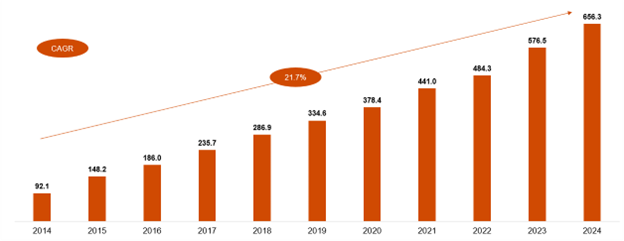

In Europe alone, private credit AuM soared from $ 92.1 in 2014 to $ 656.3bn in 2024, with a CAGR of 21.7%, reflecting a structural shift in how capital is sourced and deployed.

Figure 2. European private credit AuM ($bn)

However, European private credit still has some catching up to do with the US, where AuM stood at around $ 1.3tn in end-2024. Moreover, European private credit remains relatively small compared to bank financing. As a matter of fact, as per data from the ECB, the total stock of bank loans to corporations in the Euro Area in December 2024 stood at EUR 5,172.4bn (around $ 5,380bn) – well above the $ 656.3bn of private credit AuM in all of Europe.

An engine for yield, diversification, and real-economy impact

The growth of private credit in Europe is driven by a maturing ecosystem of fund managers, platforms, and service providers. Institutional investors seeking yield and diversification are getting drawn to the asset class’s attractive risk-adjusted returns, low correlation to public markets, and bespoke structuring flexibility. As many loans provided by private credit funds tend to have a floating rate, such attributes are seen by investors as offering rare control, resilience and attractive yields in a macroeconomic climate marked by volatility.

Mario Draghi’s landmark 2024 report for the European Commission emphasised the need to mobilise private capital more effectively, particularly for infrastructure and innovation. The report called for the completion of the Capital Markets Union/Savings and Investments Union to unlock much-needed financing for European businesses. Private credit, with its adaptability, flexibility and long-term orientation, is uniquely positioned to fill this capital gap and to spur much-needed infrastructure investments across the EU.

Moreover, an emerging generation of funds is blending financial return with sustainability goals. From funding renewable energy projects to supporting SME decarbonisation, private credit is increasingly aligned with ESG objectives, particularly when given a push from public or semi-public sources. A notable example is the Green Private Credit fund of funds, a €200 million fund recently launched by the European Investment Fund and nine French institutional investors with the aim to “boost green financing for European SMEs and small mid-caps.”

Institutional capital brings scale, sophistication, and stability to the market. These investors are equipped with advanced underwriting and monitoring capabilities, enabling them to support complex, capital-intensive projects. Their long-term horizons also provide a stabilising force during market stress.

The return of the banks – but in a new role

Interestingly, banks are not entirely out of the picture. While they initially retreated from corporate lending post-2008, many are now entering the private credit space, albeit in new forms. For instance, Europe’s largest bank, HSBC, recently committed $4 billion to its private credit funds, with ambitions to scale to a $50 billion platform within five years. Several other banks have also shown private credit ambitions via their asset management subsidiaries.

These moves reflect a broader trend: the blurring of lines between traditional and alternative finance. Banks are leveraging private credit funds’ origination and servicing capabilities while maintaining capital efficiency. However, this hybrid model complicates regulatory oversight, risk attribution and transparency, especially in co-investment or structured deals.

Not without risks

The rapid institutionalisation of private credit is not without challenges. As capital pours into the asset class, several structural vulnerabilities are becoming increasingly apparent.

While offering attractive returns and diversification, private credit operates with limited transparency and liquidity compared to public markets. The absence of standardised disclosures and active secondary trading makes it difficult for investors to assess risk, benchmark performance, or exit positions during periods of market stress. These constraints can obscure underlying vulnerabilities and complicate portfolio management, particularly in volatile environments.

A further concern is the concentration of lending to private equity-sponsored companies. A non-negligible share of private credit is directed toward these borrowers, who often benefit from experienced ownership and streamlined deal execution. However, this introduces a high degree of correlation across portfolios, and such interconnectedness could amplify systemic risks in a downturn.

Compounding these issues is the limited availability of historical default and recovery data, especially in Europe, which hampers accurate risk modelling and stress testing. This data gap increases the risk of mispricing and may lead to an underestimation of downside scenarios, particularly in less mature or less transparent markets.

Managing the risks: A call for innovation and oversight

To ensure the sustainable growth of private credit, a coordinated and forward-looking approach to managing emerging risks is needed. This begins with enhancing transparency and reporting standards. Regulators and industry bodies should advocate for standardised frameworks that improve visibility into portfolio composition, risk metrics, and performance, enabling more effective benchmarking and risk assessment across the industry.

In parallel, developing secondary markets for private credit instruments could significantly improve liquidity, allowing investors to manage risk and rebalance portfolios more effectively. While challenging, this evolution would mark a critical step toward market maturity.

Equally important is the advancement of data infrastructure and regulatory coordination. Asset managers must invest in robust analytics and data systems to overcome the limitations of historical data. Tools such as scenario analysis, stress testing, and machine learning can help uncover hidden risks and support more informed decision-making.

Private credit’s rise is reshaping capital markets, supporting the real economy, and offering institutional investors a powerful tool for yield generation and portfolio diversification.

Yet with scale comes great responsibility. To ensure long-term resilience, the industry must evolve beyond a singular focus on returns. Embracing a more holistic approach, one that integrates rigorous risk management, strong governance and sustainability principles, will be essential to navigating future challenges and maintaining investor confidence.

{kind=link}