In June 2025, the Financial Conduct Authority’s (FCA) Quarterly Consultation Paper 25/16 (CP), acknowledged it was time to review the requirements and level the playing field between Consumer Duty and Assessment of Value (AoV) rules, under the Collective Investment Schemes sourcebook (COLL).

Following the Asset Management Market Study, AoV was introduced in 2019 to increase competition and enhance transparent pricing between asset managers and investors.

Consumer Duty (initially open-end products in July 2023 and closed-end in July 2024), was introduced to provide a principles-based framework for the evaluation of delivery of good outcomes to retail customers across asset management, banking, and insurance services.

While both regulations address value for money, AoV assessment rules exceed the FCA’s Consumer Duty, creating duplication and an uneven playing field for UK Authorised Fund Managers (AFMs) distributing UK funds.

As Consumer Duty nears its second anniversary, asset managers’ grievances have grown. The three main pain points remain: how can we streamline overlap, how can we align rules for AFMs, and how can we deliver proportionate and consistent reporting?

As Consumer Duty nears its second anniversary, asset managers’ grievances have grown. The three main pain points remain: how can we streamline overlap, how can we align rules for AFMs, and how can we deliver proportionate and consistent reporting?

The consultation paper proposed to reduce and simply these detailed reporting requirements with a general requirement, where AFMs would include an annual report summary of the AoV in their annual financial reports. This would provide greater flexibility to AFMs over what they publish, share, and how they comply.

Regulation effectiveness

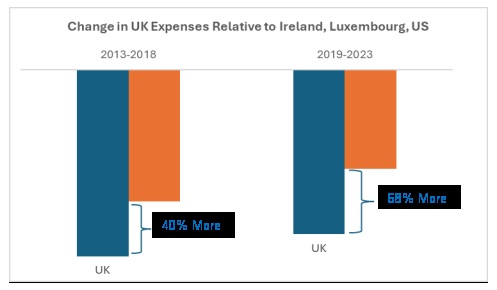

With more than five years of AoV, we can now measure its impact and efficacy on UK funds’ fees by comparing the periods immediately before and after the September 2019 launch of the Assessment of Value framework.

In a Broadridge Global Pricing Intelligence fee study, we observed that UK-domiciled funds saw average fees fall 68%* more than their closest competitors’ fee fall between 2019 and 2023, compared to a 40%* fall for the previous five years to 2018. The rate of UK fee compression post-2019 significantly exceeded its closest competitor markets in Luxembourg, Ireland, and the US.

While economic and market forces played a role, AoV’s requirements for transparent fund fees and value benchmarking have clearly demonstrated the impact enhanced regulatory measures in the UK have had on fee compression relative to other regions.

While economic and market forces played a role, AoV’s requirements for transparent fund fees and value benchmarking have clearly demonstrated the impact enhanced regulatory measures in the UK have had on fee compression relative to other regions.

Rationalising the Value-Duty gap

Considering AoV regulation is here to stay, it’s worth analysing the key challenges faced by asset managers when implementing both Consumer Duty and AoV.

- Alignment: To avoid duplicate assessments, asset managers need to map and align regulation overlap between AoV’s seven value criteria and Consumer Duty’s outcomes.

- Assessment periods: To improve comparability of management information, asset managers are required to harmonise Consumer Duty’s product lifecycle and AoV’s historical assessment periods.

- Stakeholders: Consumer Duty care extends across all market participants, while AoV rules only apply to AFMs, so maintaining equivalent standards of care and drive collective accountability across the distribution chain is a challenging process.

- Publishing: Replacing the annual AoV statement with the new AoV summary as proposed in the Consultation Paper, asset managers will be required to determine what constitutes “sufficient reporting”, increasing governance burdens on fund boards.

- Board independence: AoV requires two independent directors or 25% of an independent board, while Consumer Duty has no thresholds. Harmonising board governance standards would ensure consistent oversight and value delivery.

- Offshore asset managers: UK-distributed funds should uphold the same duty of care, regardless of domicile. Under the Overseas Fund Regime’s equivalent protection principles, offshore managers are exempt from AoV and often delegate Consumer Duty compliance to UK distributors.

Complexity to clarity

In the FCA’s Consultation Paper 25/16, the FCA proposes to simplify COLL’s AoV reporting by replacing the annual AoV statement with an AoV summary disclosure in annual reports.

Amid industry headwinds, market volatility, and compliance pressures, these reforms offer welcome relief. Yet as COLL and Consumer Duty still demand clear duty of care and value for money services, the FCA should use this consultation to tackle broader challenges-clarifying requirements, aligning governance, and levelling the onshore-offshore playing field.

Rationalising non-value-added requirements through best practice implementation guidelines will bring collective accountability and serve as a much needed tonic to boost the UK domiciled fund management industry, which reached $2.4trn* (£1.7trn) in AUM in June 2025 for mutual and hedge funds ($2.8trn (£2.1trn) including investment trust, pension and insurance funds), underpinning the UK’s global leadership and aspirations for future growth.

*Source: Broadridge’s Global Market Intelligence and Global Pricing Intelligence.

{kind=link}