However, the tides are shifting. Retailisation—or ‘democratisation’—is gradually tearing down barriers and inviting everyone to the table. We are witnessing not just a trend, but a transformation that will recalibrate the asset management industry and cement the position of alternative investments within it.

But why now? Firstly, investors’ attention is being drawn by the prospects of higher yields. But there is more to this hunt than just returns—a younger socially conscious and tech-savvy generation of investors is emerging, drawn to the opportunities for diversification and measurable impact which private markets offer.

However, this momentum is not just about expanding access. Policymakers and regulators across Europe are realising the need to open private markets to wider swathes of investors to channel more capital towards essential sectors of the European economy, such as housing and renewable energy. European businesses, long dependent on a banking sector that heavily became risk-averse since the Global Financial Crisis, will now have access to fresh sources of capital.

Europe is at the forefront of alternative investments’ democratisation, yet its progress is dogged by regulatory hurdles amongst other barriers. European asset managers must grab this opportunity or be left in the dust.

Private markets for all: Where do we stand?

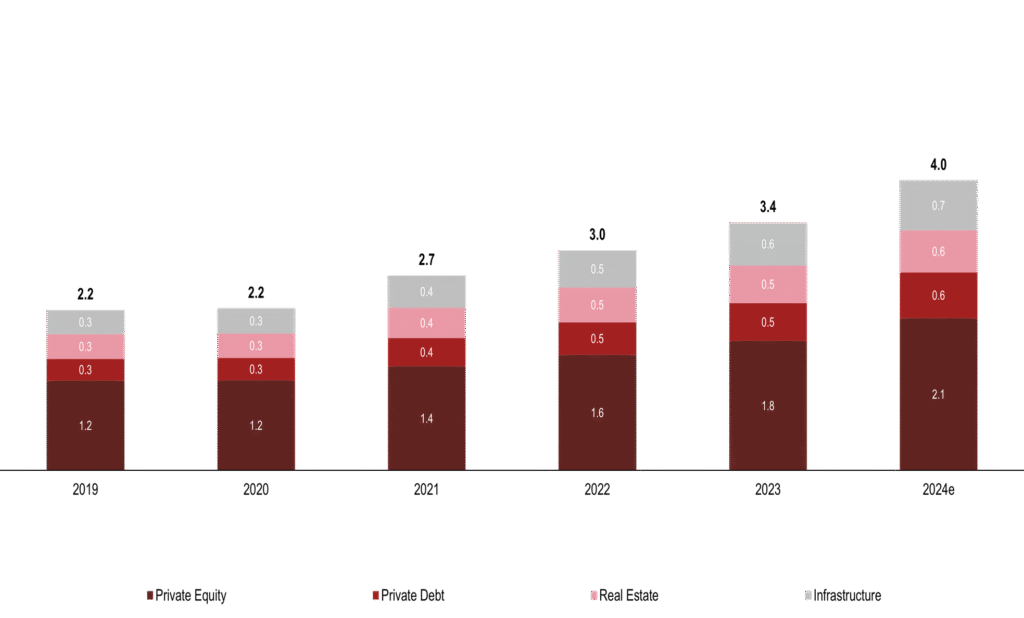

The numbers speak for themselves. As of Q4 2024, alternative assets under management (AuM) in Europe are estimated to have reached €4 trillion, spread across the private equity, private debt, infrastructure, and real estate asset classes. This is almost double the amount recorded for 2019 (see Figure 1).

Figure 1. European Private Markets AuM by Asset Class (€ tn)

Sources: PwC Global AWM & ESG Research Centre, Preqin, Monterey.

For now, institutional investors still dominate the alternatives segment, and retail investor participation may still be at its pilot stages. But the capital flowing into alternatives is undeniable and tells a story of huge opportunity for growth—with tokenised assets on a slow but steady path to expand access.

Blackstone’s pioneering European Private Credit Fund—which introduces a retail-focused alternative product—is a prime example of the transformation underway in the European asset management industry. The walls around private markets are slowly being breached—backed by regulatory and policy momentum, technology, and investor demand.

What is driving this transformation?

Regulatory frameworks such as the recently updated European Long Term Investment Fund (‘Eltif 2.0’) and the UK’s Long-term Asset Fund (LTAF) are not only presenting retail investors with more opportunities for entry, but also ensure more protections.

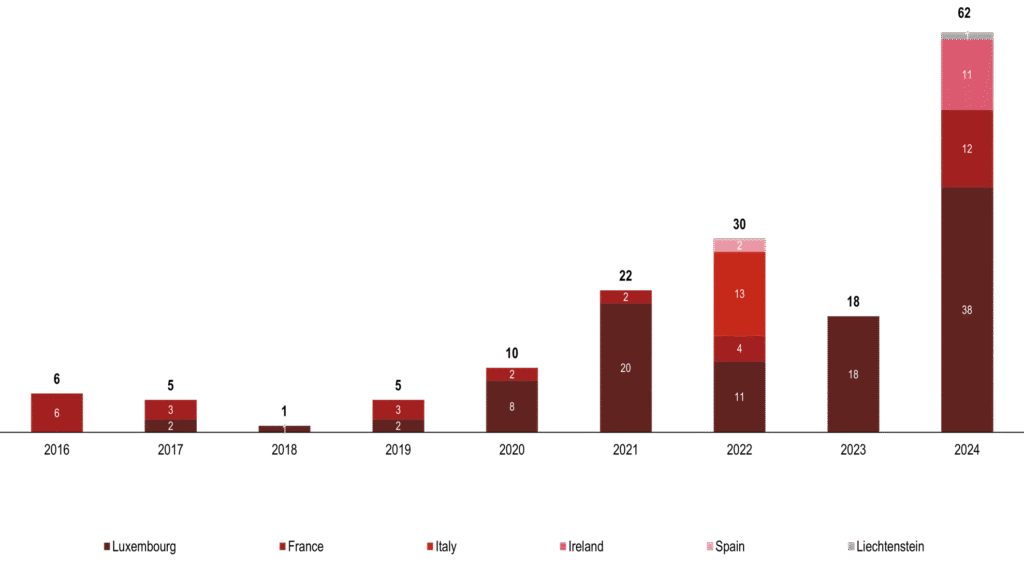

However, while regulatory and policy momentum is building, progress across Europe remains uneven. Take France for example, where Eltifs must be registered domestically to qualify for life insurance contracts—a crucial point for retail investors. This extra layer of complexity has pushed many asset managers to look elsewhere, with many turning to Luxembourg, which has cemented its place as the go-to hub for Eltif registrations thanks to a streamlined framework and robust platform offering better flexibility (see Figure 2).

This underscores a critical issue—harmonisation in Europe is still a work in progress and until regulatory alignment is improved, asset managers will have to choose their jurisdiction wisely to unlock the full potential of Eltifs.

Figure 2. Number of Eltifs Launched by country (Europe)

Sources: PwC Global AWM & ESG Research Centre, Esma

Apart from these promising regulatory developments, the rise of blockchain and tokenisation is also changing the way private assets are owned and traded. Thanks to blockchain-powered fractional ownership, retail investors can hold pieces of high-value alternative assets—from real estate to fine art.

But while the democratisation potential is immense, roadblocks remain. One of the biggest is the steep learning curve for retail investors navigating the illiquid and complex nature of private market investment. In addition, understanding the complex web of global and regional tokenisation regulations can be a daunting task, which requires asset managers to tread carefully and stay ahead of regulatory developments as they embrace this shift.

What is next: Adapt or get left behind

The shift towards alternatives is no longer on the horizon—it is here, and having a foothold in alternatives and private markets is becoming a sine qua non for asset managers. With global alternatives AuM expected to reach US$27.6 trillion by 2028, as per PwC’s latest Asset and Wealth Management Revolution report, the writing on the wall is clear. Even BlackRock—the biggest ‘traditional’ asset manager in the world— acquired a major private markets player in 2024, symbolically highlighting that alternatives are not optional but essential.

However, while identifying the shift is one thing, being able to harness it for sustained success is another. To stay ahead, asset managers must embrace democratisation with strategic intent. Digital platforms need to be improved via collaborations with fintechs who—adept at utilising cutting-edge technology—are improving financial services and creating innovative solutions to enhance access to retail investors.

Liquidity remains a sticking point, but semi-liquid structures like the aforementioned Blackstone fund—which allow periodic redemptions—would go a long way to boost retailisation in private markets. Meanwhile, private markets ETFs and tokenisation offer liquidity by breaking down high-value investments into smaller, tradeable units, in essence democratising them and improving access to retail investors.

The way forward for asset managers is clear: innovate and adapt to the democratisation of the alternatives segment, or risk getting left behind.

{kind=link}