Mamdouh Medhat PhD, a senior researcher at Dimensional Fund Advisors, considers whether corporate bonds have a place in a portfolio that already holds government bonds and equities.

Research finds that investment-grade corporate bonds have a relatively low correlation with equities, meaning investors can expect a higher return, without increasing volatility, by adding corporate bonds to a multi-asset portfolio.

Both bonds and equities suffered declines in 2022. This prompted an examination of the relation between the two asset classes and what role they may play together in a balanced or multi-asset portfolio. Many such analyses limit themselves to the correlation between stocks and low-risk government bonds. My research colleagues, Aabbhas Garg and Samuel Wang, take that a step further by considering the specific role of corporate bonds in stock and bond portfolios.

While corporate bonds have higher volatility than government bonds, they have lower volatility than stocks. For an equity-heavy asset allocation, adding investment-grade corporate bonds to the fixed income mix can improve expected returns without significantly impacting overall portfolio volatility.

Still, some investors may question the usefulness of adding corporate bonds to a portfolio dominated by stocks. In particular, they may think there is a high correlation between the returns of stocks and corporate bonds, especially since many corporate bonds are issued by companies that also issue equity.

Asset pricing theory tells us that we can conceptually think of a corporate bond as a combination of buying a risk-free bond and selling a “put option” on the company’s assets with a “strike price” equal to the face value of the company’s debt (a put option is the right to sell an asset at a future date for a predetermined price, called the “strike” price).

For an investment-grade bond, the put option has a near-zero value because the strike price is lower than the market price of the underlying asset. But in the case of a high-yield bond, the value of the put option is not negligible and the asset value plays a big role in the bond valuation. Thus, theory says that compared to a high-yield bond, an investment-grade bond should be less correlated with the firm’s asset value and, hence, its equity value.

Research

This is what Garg and Wang set out to test and quantify in the data. They mapped corporate bonds to the stocks of their issuers and used this mapping to estimate the correlation between stock and bond returns.

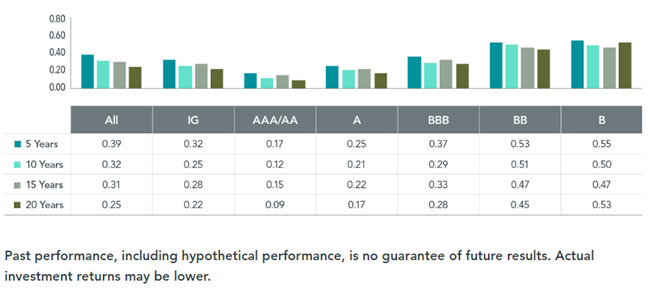

As a first step, they computed the correlation between each issuer’s monthly bond and stock returns for the five-, 10-, 15-, and 20-year periods ending in December 2020. Because companies can issue multiple bonds, Garg and Wang calculate monthly bond returns as the value-weighted average return across all bonds belonging to the same issuer. They then took the cross-sectional average of these correlations across all issuers as well as across issuers’ initial credit ratings. The results of this exercise are reported in Exhibit 1.

The average correlation across all issuers (the “All” column) is relatively low, ranging from 0.25 over 20 years to 0.39 over five years. Breaking down these results by credit rating shows that the correlations tend to increase as credit quality worsens. For example, the average correlation over the five years ending in December 2020 is 0.17 for AAA/AA-rated issuers, yet 0.53 and 0.55 for BB and B-rated issuers, respectively.

Correlation between corporate bonds and stocks

Cross-sectional average of correlations between corporate bonds and stocks for periods ending in December 2020

Exhibit 1

Source: Issue-level bond data and stock data provided by Bloomberg.

Source: Issue-level bond data and stock data provided by Bloomberg.

As a second approach, they calculate the correlation between the stock and bond portfolios of the mapped issuers. Each month, bond portfolios of different credit ratings are constructed using bonds that are mapped to their issuing companies, while the associated stock portfolios consist of the stocks of all the issuers of eligible bonds in the respective bond portfolios. The portfolios are value-weighted and rebalanced monthly.

Exhibit 2 shows the correlations between the corporate bond and stock portfolios over time. Unsurprisingly, the overall portfolio correlation is relatively low (0.42). The correlations between investment-grade-rated corporate bonds and stocks range from 0.08 to 0.42, while they are higher (0.68–0.74) between high-yield corporate bonds and stocks.

Correlation between corporate bond and stock portfolios

Correlation between corporate bond portfolio and associated stock portfolio, January 2001 – December 2020

Exhibit 2

Source: Issue-level bond data and stock data provided by Bloomberg.

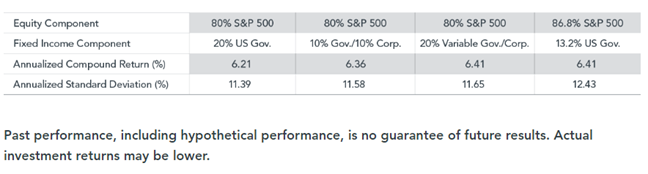

The low correlation between stocks and investment-grade corporate bonds can benefit investors in a multi-asset strategy. Using the 80% equity/20% fixed income allocation as an example, Exhibit 3 shows that adding investment-grade corporate bonds increases the portfolio’s expected return from 6.21% to 6.36% annualized without a meaningful increase in volatility (from 11.39% to 11.58%).

But this is not all. As Exhibit 3 also shows, applying a variable government/credit approach to the allocation in the fixed income component, which dynamically increases the allocation to corporate bonds when credit spreads are wide but scales it back when credit spreads are narrow, can further increase expected returns to 6.41% annualized. Since this comes with a volatility of 11.65%, it compares favourably to the static strategies. Lastly, if you were to replicate this higher return (6.41%) using a balanced strategy with only stocks and government bonds, you would need to increase the stock allocation to 86.8%, which results in about 1% higher volatility.

Summary Statistics of 80% equity/20% fixed income balanced asset location

80% equity/20% fixed income allocations with different weights in corporate bonds, January 2001 – December 2020. Returns in USD

Exhibit 3

Source: Equities represented by SP 500 Index.

In summary, analysis shows that investment-grade corporate bonds have relatively low correlations with stocks and can help target higher expected returns without substantially increasing the portfolio volatility in a multi-asset strategy.

© 2023 funds europe

{kind=link}