As the war between Iran, the US and Israel enters its second month, insights from the asset management community continue to point to uncertainty in outcomes – as, for example, analysts warn that even if the ‘hot’ war moves towards a solution, the energy shock impact could be lingering.

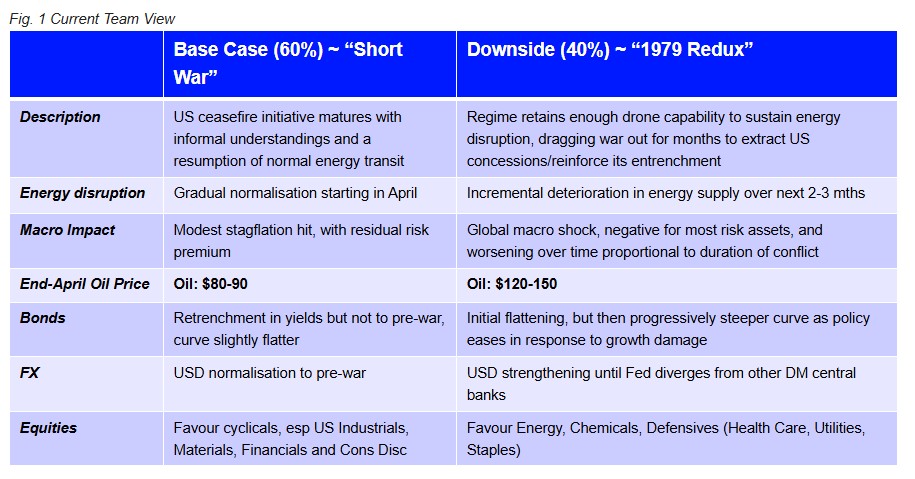

Elliot Hentov, chief macro strategist at State Street Investment Management has put out the following table, suggesting a 60%/40% split in risk between a return to the mean versus an extended period of deterioration:

The Lazard Geopolitical Advisory team outlines its expectations thus:

- Scenario 1: Substantive Agreement

The Strait reopens gradually within ~2–4 weeks of a ceasefire. Traffic can then normalise faster, contingent on insurer re-entry, shipowner confidence, and early movers catalysing broader market participation. Energy prices remain above pre-war levels for several months before easing as markets gain confidence in the durability of the agreement and flows and production normalise. - Scenario 2: Declared Victory / Limited Ceasefire

Traffic restarts within ~4–6 weeks of a declared victory, but flows remain subdued as the absence of a more substantive agreement and an unresolved conclusion leave the security environment fragile. Energy prices remain elevated for longer than in Scenario 1, as markets struggle to fully price out risk given the lack of a durable settlement. - Scenario 3: Simmering Conflict

Traffic through the Strait remains largely closed until a gradual, partial reopening over 4-8 weeks due to military escorts, with capacity remaining below normal levels for the foreseeable future. Energy prices remain highly volatile, with Brent fluctuating between ~$90–150/bbl., rising toward the upper bound the longer shipping disruptions persist and inventories and temporary buffers are depleted. - Scenario 4: Energy War

Traffic is effectively shut with closure potentially lasting 3–6 months, as both the Strait and alternative export routes remain disrupted. Energy prices surpass $150/bbl. with persistent supply shortfalls driven by damage to Gulf energy assets.

Aviva Investors notes that “The duration of time that the Strait of Hormuz remains closed will be pivotal to the global growth outlook for the remainder of 2026.”

“Aviva Investors’ Investment Strategy team have revised down their central case for global growth to 2.75 per cent for 2026, down around 0.2 per cent from the start of the year. This is a result of rising energy prices.”

“The team note there are a range of outcomes for the global economy, and that uncertainty could persist for many months, leaving visibility impaired and the global economy once again struggling to respond to a negative supply shock.

“A key aspect will be the impact on headline inflation, with the predicted drag on growth primarily reflecting the inflationary impacts of higher energy prices. The team’s central scenario is that headline rates of inflation in 2026 are now expected to be around 1-1.25 percentage points higher than forecast at the start of the year. For the US, EZ and UK, this means inflation is now expected to rise this year, rather than fall, peaking around 3 per cent and only moving meaningfully back towards target in 2027.”

Michael Grady, head of investment strategy and chief economist at Aviva Investors, commented: “The conflict in Iran and the closure of the Strait of Hormuz have changed the global picture and reshaped the expectations for global growth, inflation and interest rates this year. There is now a high level of uncertainty across markets and a wide range of possible outcomes. As a result, a more cautious to tactical asset allocation is required at this time to ensure that portfolios are robust to that range of outcomes, while remaining agile in response to developments.”

Additionally, Susannah Streeter, chief investment strategist at Wealth Club, a UK investment service for high net worth and sophisticated investors, points to the social cohesion risk now starting to appear in G7 countries such as the UK

“With oil prices having headed sharply higher again, it is not surprising motorists are reacting and stocking up on fuel, with further hikes at the pumps expected. The warnings that crude prices could hit $150 a barrel if the war continues for many weeks or even months are a highly troubling prospect. Qatar forecast that possibility and Iran has warned that crude prices could even hit $200 a barrel. Given the destruction of energy facilities and the ongoing blockade of the Strait of Hormuz, any big retreat in crude prices looks unlikely right now. However, there are no shortages of supply, and panic at the pumps will cause even more problems. While filling up for regular use may be sensible, with motorists carting off multiple containers of fuel, there’s a risk stations will run dry causing knock on effects for communities.”

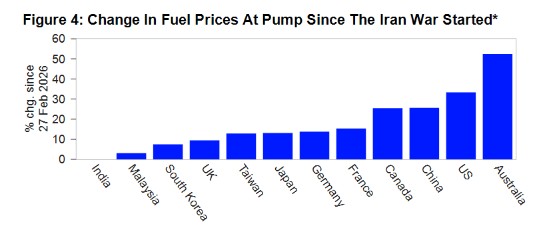

According to State Street Investment Management data, Australia has seen some of the biggest hikes in pump prices among developed markets.

{kind=link}