Mid-sized managers face a unique cocktail of AUM growth and profitability challenges, according to data put forward by Broadridge at the latest ALFI Global Asset Management Conference.

Nabeel Ansari, senior director, Broadridge Financial Solutions, who presented the findings – and moderated a panel on the challenges facing mid-sized managers – outlined the structural challenges including:

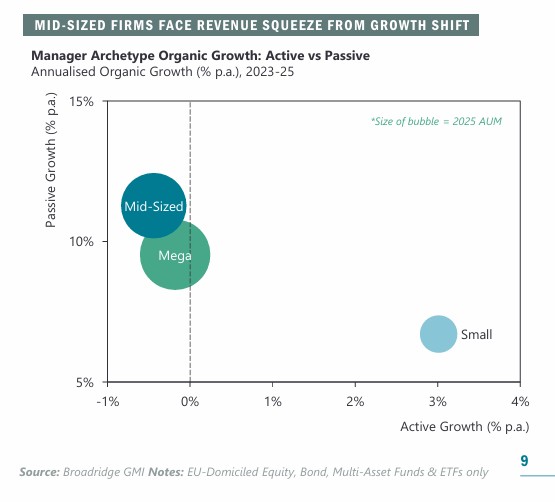

- Passive encroachment in Europe continues to capture wallet share and outpace active growth, this is where mid-sized firms are seeing strongest growth

- Active product sets are often either too narrow to deepen share of wallet with a client, or too broad to sustain clear differentiation

- Firms face greater execution risk than larger peers, given persistent margin pressure and more limited organisational capacity

- Rising demand for tailored solutions from an increasingly sophisticated investor base places further strain on resources and profitability

On organic growth, Ansari commented that the larger firms are better able to leverage the growth in passive, while for specialist boutiques, the focus of growth continues to be active.

“Passive growth is about scale,” he said. This makes it harder for mid-sized managers to compete with the largest firms.

But unlike the boutiques, they may also not be best placed to capture growth from active. It is harder to differentiate from the specialists, he noted.

From a top line perspective, the question arises whether mid-sized managers are facing concentration risk regarding their source of profitability: if it is focused on too few products, this presents risk.

These managers also do not have the pockets to fund expansion geographically in the same way as the larger firms. They do not have the same capacity to absorb failures, such as going into a new market, only to have to subsequently pull back when business growth is lacking. Larger firms can absorb more such challenges on the balance sheet.

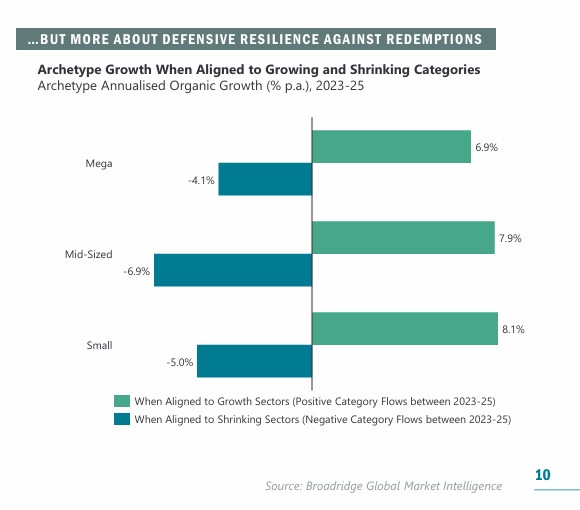

Another point made is that while mid-sized firms can capture assets flowing into sectors when subscriptions grow, the key challenge lies in periods of outflows – redemptions – taking place in particular sectors; when that happens, it tends to be the mid -ized managers that experience greater outflows than either the larger players or the specialist boutiques, Ansari commented on the data.

The boutiques get a form of “forgiveness” from their investors – including institutions – who may have deeper relationships and understand that strategies can go through peaks and troughs.

{kind=link}