[SPONSORED CONTENT}

1.

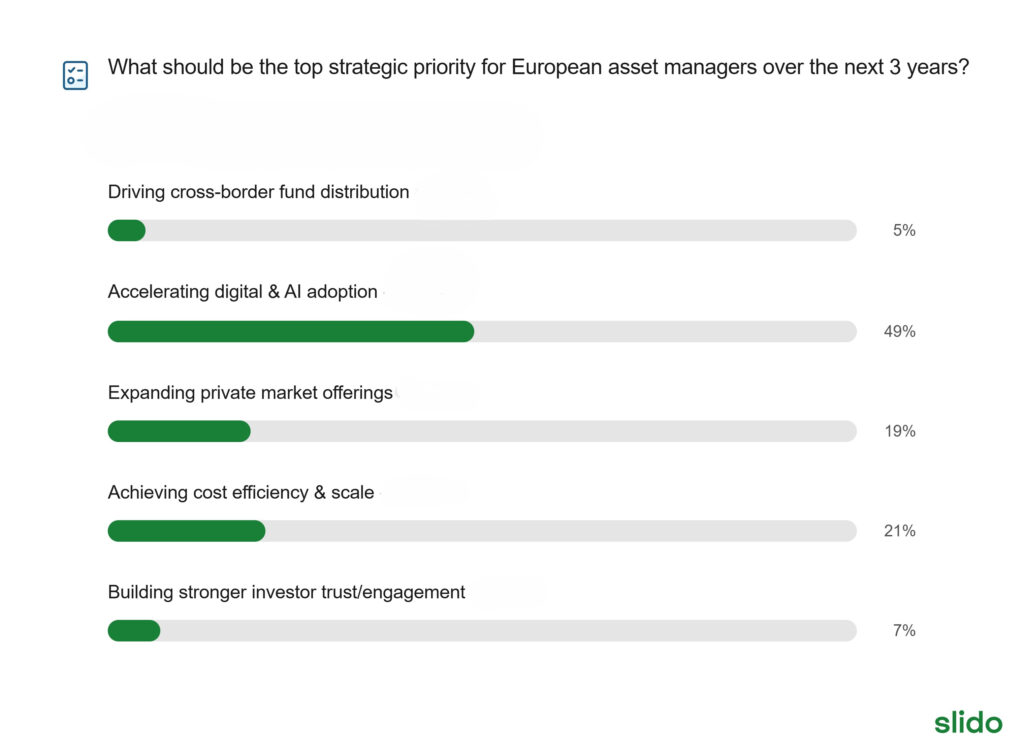

Digital and AI adoption is the industry’s top priority according to almost half (49%) who answered this question. Other priorities include cost efficiency and scale (21%) just shading expanding private market offerings (19%).

2.

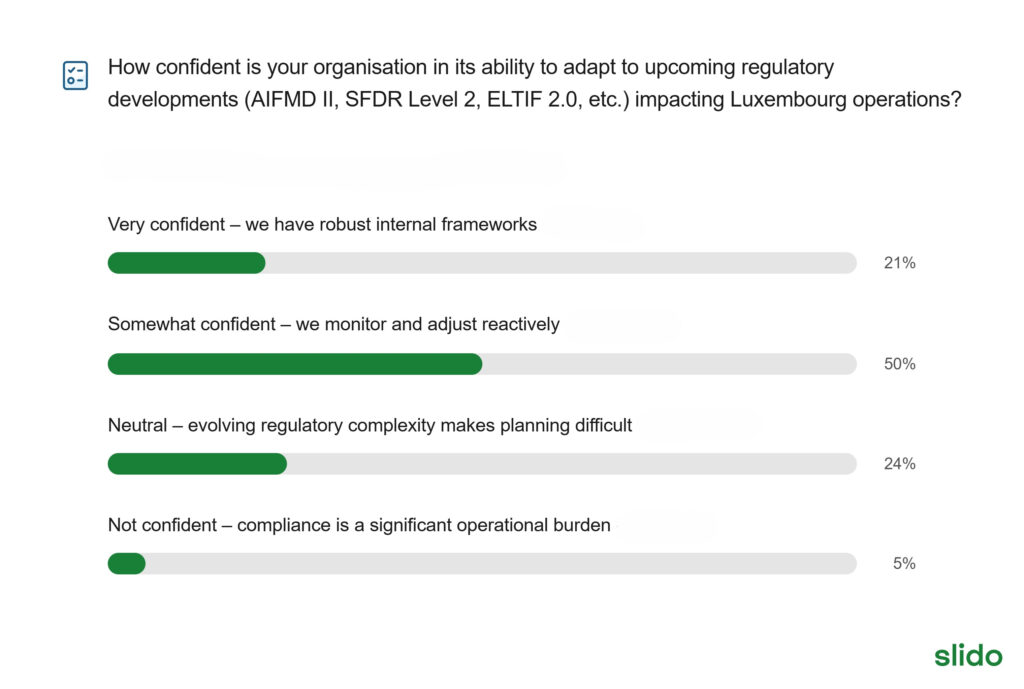

Confidence was evident in that most were either very (21%) or somewhat (50%) confident in their abilities to adapt to upcoming developments as they may affect operations in Luxembourg – such as AIFMD II, SFDR Level 2 or ELTIF 2.0.

3.

3.

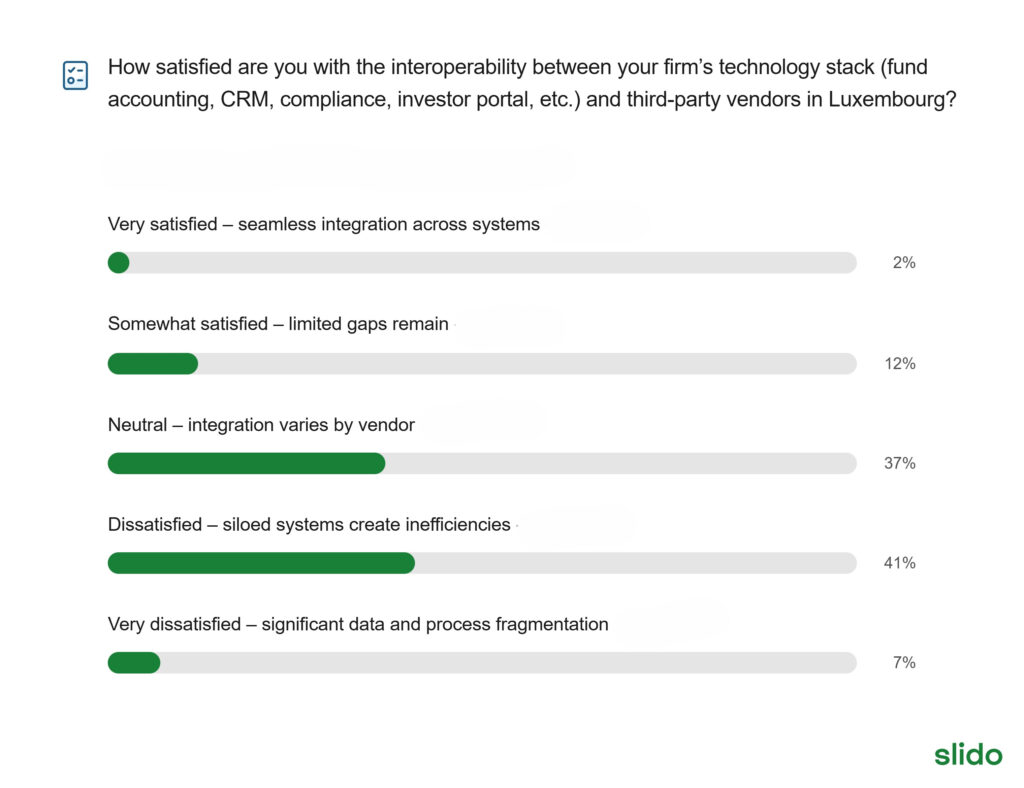

More technological complexity may explain a tilt towards respondents feeling dissatisfied (41%) or neutral (37%) at best about interoperability with third-party ventors.

4.

4.

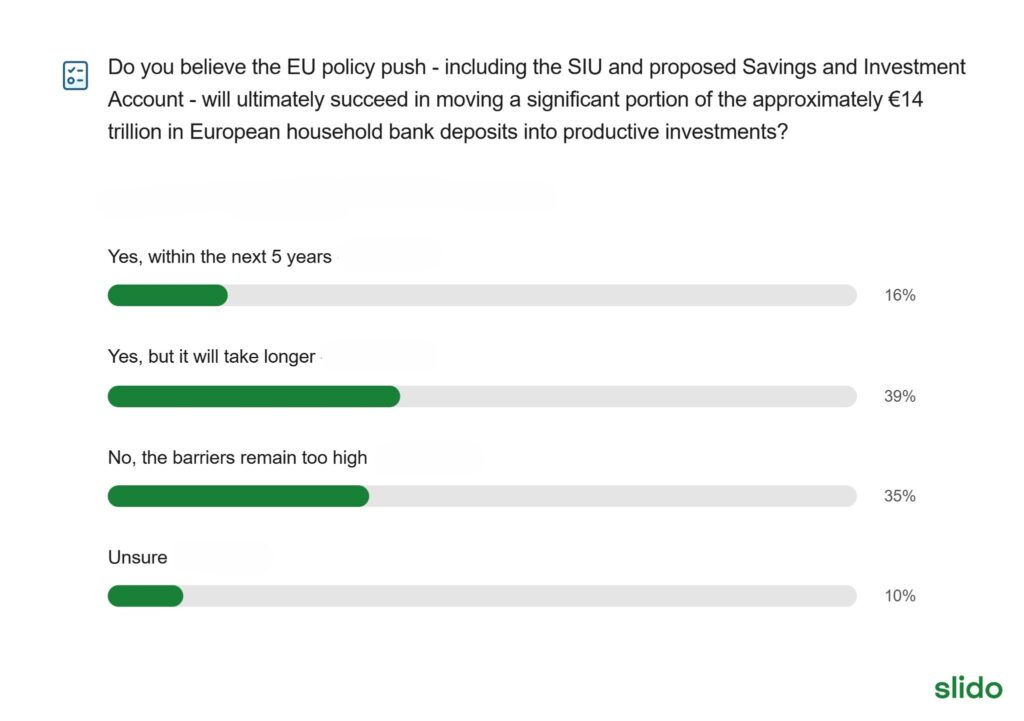

The SIU may succeed, but either take more than five years (39%) to accomplish or may never take off because the barriers remain too high (35%), the majority answered.

5.

5.

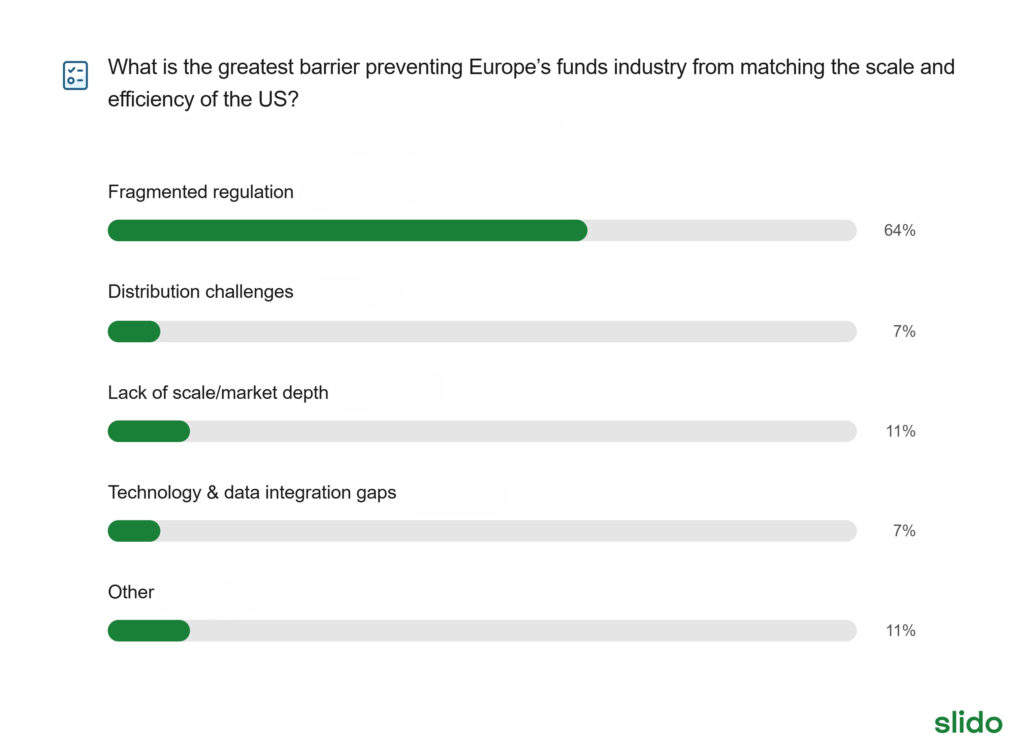

The EU through the European Commission may be trying to find ways to reduce friction in the single market. But according to the results seen in the polling, there is much still to be done by the policy makers and regulators in Europe to achieve industry scale and efficiencies equal to the US. Respondents see fragmented regulation (64%) by far as the biggest barrier to achieving this. At 11% of responses, lack of scale/market depth per se in Europe is not seen as significant barrier, nor are distribution challenges (7%) or technology and data integration gaps (also 7%).

6.

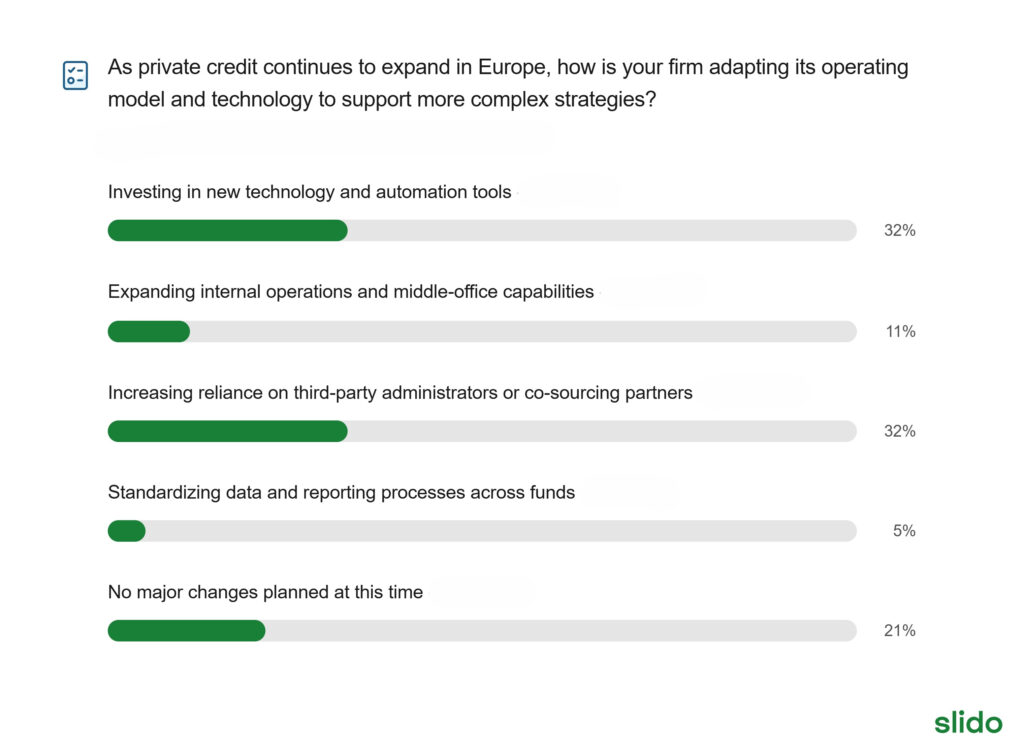

As the event considered the accessibility of private markets assets through the ELTIF 2.0 vehicle, the related poll for delegates focused on private credit, and the

importance of operating models and technology support. Answers point to an industry both investing in new technology and automation tools (32%) and increasing reliance on third- party administrators or co-sourcing partners (32%), while about a fifth (21%) said that they were not planning major changes. Standardising data and reporting processes across funds (5%) was not seen as important.

7.

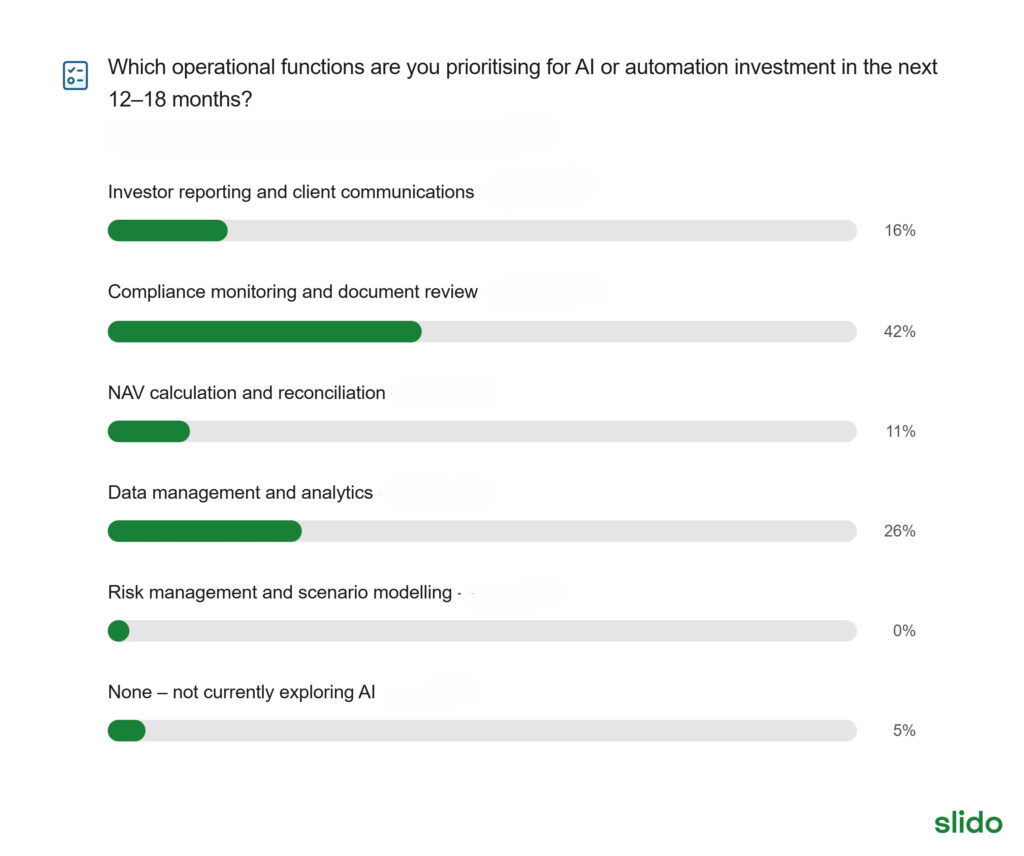

Continuing on the data point, the subsequent live poll during the event asked about investment priorities in AI or automation in fund operations over the coming 12-18 months. Compliance monitoring and document review (42%) scored highest among respondents, although data management and analytics (26%) and investor reporting and client communication (16%) were also seen as relatively important. Interestingly, despite the volume of discussion around AI in the industry generally, here 5% responded that they are not currently exploring AI in respect of operational functions.

8.

8.

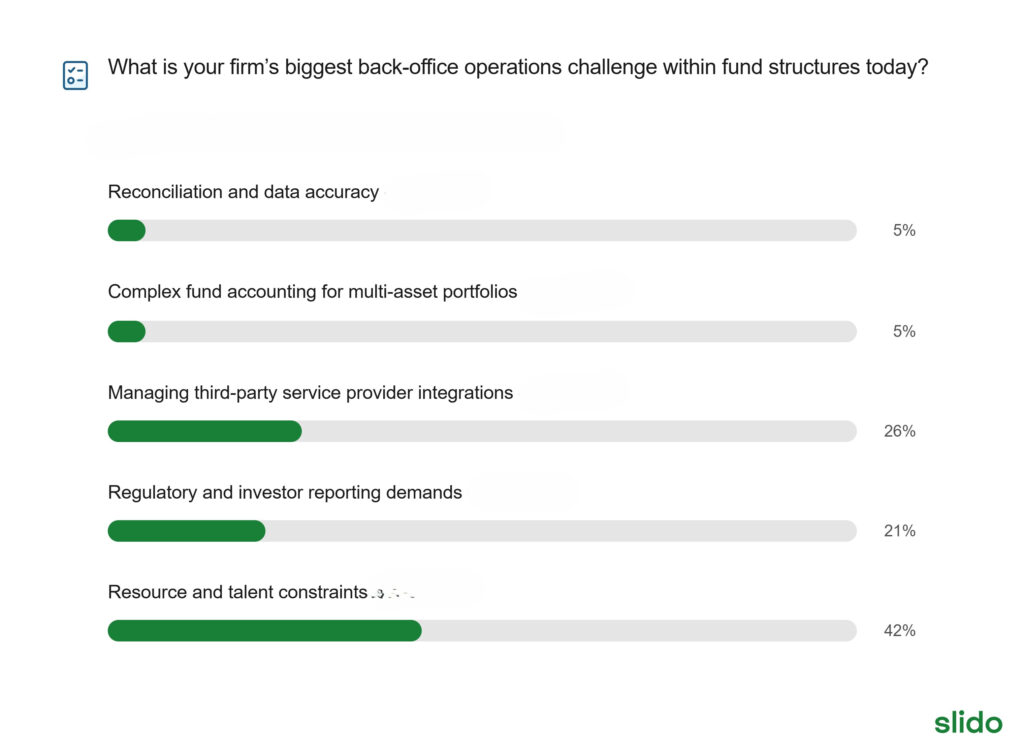

The final audience poll concerned perceptions of back office operations challenges. Here, resource and talent constraints (42%) stood out – reflecting perhaps ongoing discussion on finding the best experts to hire at a time when AI is being increasingly incorporated into processes, or simply that it is hard to find talent. Managing third-party service provider integrations (26%) stood out as third party-related issues did in some previous poll answers. And the need to respond to regulatory and investor reporting demands (21%) continues.

{kind=link}