Funds Europe presents data about some of the specialist fund administrators that oversee assets for private equity and real estate investors in Europe. There is also a directory of providers and a Q&A with a number of the firm’s senior executives. Meanwhile, Nicholas Pratt speaks to administration specialists within the cross-border fund domiciles that have been launching fund structures to help alternative fund managers cut back on regulatory red tape and get to market quicker.

A number of European domiciles have launched ‘manager-led’ fund structures in order to attract professional and institutional investors in specialist fund classes, such as real estate and private equity.

Whereas the Alternative Investment Fund Managers Directive (AIFMD), introduced a stiffer regulatory regime for Europe’s alternatives fund market, the new structures are designed to strip back some of the oversight and provide a more streamlined regulatory framework for investors that should be sophisticated enough to do their own due diligence.

Whereas the Alternative Investment Fund Managers Directive (AIFMD), introduced a stiffer regulatory regime for Europe’s alternatives fund market, the new structures are designed to strip back some of the oversight and provide a more streamlined regulatory framework for investors that should be sophisticated enough to do their own due diligence.

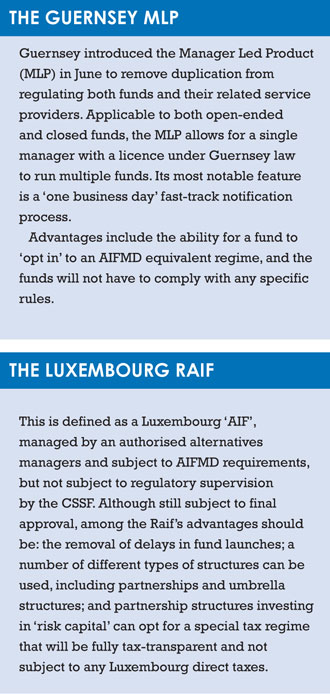

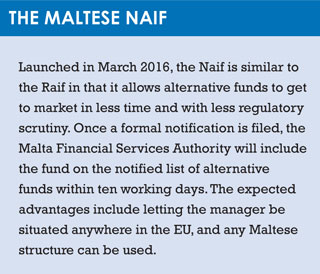

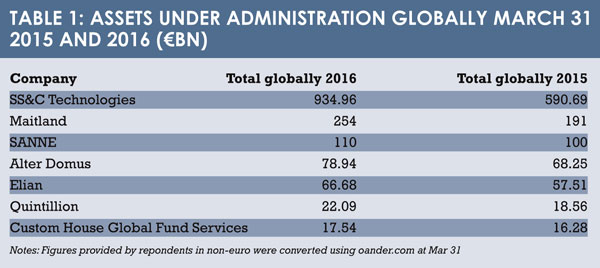

Ireland was the early mover, launching the Irish Collective Asset-management Vehicle (Icav) in January 2016. Guernsey then came out with its Manager Led Product (MLP) in March, followed by Malta and the Notified Alternative Investment Funds (Naif) and Luxembourg with its Reserved Alternative Investment Fund (Raif), which was passed into local law in July.

Meanwhile Jersey is currently in the throes of developing its own manager-led fund structure, the JRAIF. According to Mike Byrne, chairman of Jersey Funds Association, the JRAIF will make Jersey’s regime “clearer, simpler and more streamlined”.

Given that all these new fund structures are so embryonic, it is difficult to judge the level of interest as measured by assets under management or new fund launches, though Ireland’s Icav has been active the longest and, according to the latest Central Bank of Ireland figures published at the end of July, 271 Icavs have been authorised since March 2015, including by the fund-of-funds manager Permal, which relocated $4 billion worth of assets from the British Virgin Islands to Ireland in March last year.

Ireland has built up a solid reputation as a fund centre for hedge funds and several features of the Icav are designed to attract US investors, such as a tick-the-box feature for tax arrangements.

Luxembourg, Malta and the Channel Islands are hoping the new fund structures will attract investors in real estate and private equity funds that have been put off by paperwork created by the AIFMD.

Luxembourg, Malta and the Channel Islands are hoping the new fund structures will attract investors in real estate and private equity funds that have been put off by paperwork created by the AIFMD.

“With all the regulation there has been, jurisdictions are looking to be more innovative and attractive to investors,” says Kavitha Ramachandran, senior manager, business development and client management at fund administrator Maitland.

“There was a feeling that the AIFMD created a lot of duplicate regulation at both the manager and fund level. So the industry has come together to make it possible to convert funds from one regime to another and to make it easier to launch new funds under these new structures.”

LOGICAL THINKING

The logic behind these new, so-called manager-led products is that if the manager is regulated under the AIFMD, it should not be necessary to regulate each individual fund the manager launches. For example, with the Raif, there is no need to seek regulatory approval from Luxembourg’s financial regulator, the Commission de Surveillance du Sector Financier (CSSF), for a new fund launch if the manager is complaint with the AIFMD.

Clearly the domiciles that have launched new fund structures are competing with each other, but also with other onshore and offshore jurisdictions that have applied a light regulatory touch to private equity and real estate funds. For example, the Securities and Exchanges Commission in the US has little regulatory oversight for alternative funds, while the UK has a rigorous process for approving fund managers, but approval for funds is largely limited to ensuring compliance with the AIFMD.

Clearly the domiciles that have launched new fund structures are competing with each other, but also with other onshore and offshore jurisdictions that have applied a light regulatory touch to private equity and real estate funds. For example, the Securities and Exchanges Commission in the US has little regulatory oversight for alternative funds, while the UK has a rigorous process for approving fund managers, but approval for funds is largely limited to ensuring compliance with the AIFMD.

The likes of the British Virgin Islands and the Cayman Islands may feel most threatened by the new manager-led fund structures from European domiciles and the prospect of more re-domiciliations of funds.

It is unlikely though that other mainland European domiciles will follow suit with new manager-led fund structures given that the likes of France and Germany are heavily domestically focused and have fewer alternative products.

However, there are some new EU-wide structures in the pipeline, such as the European Long Term investment Fund.

“It is quite difficult to predict how other EU jurisdictions will react to attract international asset managers always seeking flexible investment structures and to improve time-to-market,” says Virginie Gonella, managing associate at the Luxembourg office of law firm Ogier.

“It is quite difficult to predict how other EU jurisdictions will react to attract international asset managers always seeking flexible investment structures and to improve time-to-market,” says Virginie Gonella, managing associate at the Luxembourg office of law firm Ogier.

“Nonetheless, it is clear that for all EU jurisdictions historically subject to ‘product supervision’, the risk of a shift away in favour of other attractive fund domiciles with a lighter regulatory burden must be taken seriously.”

Responsibility for product governance falls squarely on fund managers and due diligence on investors. The talk of innovation and ‘light touch’ regulation may sound like a worrying development in terms of investor protection but, Ramachandran says, it is simply a case of looking at new ways of doing things.

Responsibility for product governance falls squarely on fund managers and due diligence on investors. The talk of innovation and ‘light touch’ regulation may sound like a worrying development in terms of investor protection but, Ramachandran says, it is simply a case of looking at new ways of doing things.

“We adapt to new regulation and we introduce new products. Luxembourg is a classic example. It never had unregulated products before but I think it is the right way to go.

“As long as you have a regulated framework with investor protection at the top, its OK.”

NOT A BAD REACTION

Fund administrators are also keen to stress that the new fund structures do not represent reaction to tougher regulation.

Dirk Holz, real estate and private equity product management at RBC Investor & Treasury Services, says: “Reaction is a strong term, although there was certainly some frustration over the AIFMD with the time taken for fund approval, and which is largely addressed by these structures. However, the regulation and oversight on AIFMD funds is equal for all fund structures.”

The Raif, for example, allows for a fund to be in place without formal approval from the CSSF as long as the fund manager is regulated.

“Perhaps it is better to consider them an extension of the AIFMD, more targeted and appropriate for well-informed or qualified investors,” says Holz.

Although funds do not have to be approved by regulators, fund managers still need to appoint a local administrator and depositary and, in the absence of direct regulation for each fund, the appointed service providers will take on an added responsibility, says David Bailey, managing partner at Augentius.

Although funds do not have to be approved by regulators, fund managers still need to appoint a local administrator and depositary and, in the absence of direct regulation for each fund, the appointed service providers will take on an added responsibility, says David Bailey, managing partner at Augentius.

“As an administrator, we are regulated and we also have a responsibility to investors. The AIFMD uses this responsibility, as do other regulations. So they are using the professionals as their eyes and ears. We work on behalf of the fund’s investors. The fund pays our fees so that means the investors are paying them so they are our clients, essentially.”

He adds: “There is more responsibility on administrators, but it does not change the way we work.”

©2016 funds europe